Emergency Savings Habits in 2025: Cash, Credit, or Nothing at All?

October 22, 2025

Current economic uncertainty is causing many consumers to reassess their financial safety nets. Are they relying on emergency savings, turning to credit, or going without?

In this article:

- Introduction

- Key Findings

- Consumers Claim To Prefer Cash — But Credit Is the Real Safety Net

- Most Consumers Would Reach for Plastic To Cover a $500 Emergency

- Two-thirds of Consumers Have 6 Months or Less in Savings

- Emergency Savings: What We Say vs. What We Have

- Young Adults Lean on Credit for Financial Security

- Gen Z Most Likely To Go Over Their Credit Limit in an Emergency

- 76% of Consumers Don’t Have an Emergency Credit Card

- Gen Z and Millennials Embrace Digital Payments Over Traditional Methods

- Methodology

- Fair Use Policy

Introduction

In 2025, economic uncertainty has reached record highs, causing many consumers to reassess their financial safety nets. But are they relying on emergency savings, turning to credit, or simply going without? Credit One Bank surveyed over 1,000 consumers1 to learn how people are preparing — or not — for financial shocks in an increasingly unpredictable economy.

Key Findings

51% of consumers rely on a credit card to cover a $500 emergency expense

Two-thirds of consumers lack 6 months of emergency savings, with Gen X leading

Nearly 3 in 4 consumers would need a credit card to survive a financial emergency, but only 1 in 4 actually have one set aside for that purpose

1 in 4 Gen Z and millennials say they’d max out their credit cards to cover a financial emergency

62% of Gen Z have no emergency savings, nearly double the rate of baby boomers

1 in 6 consumers say they don’t have — and don’t plan to start — an emergency fund

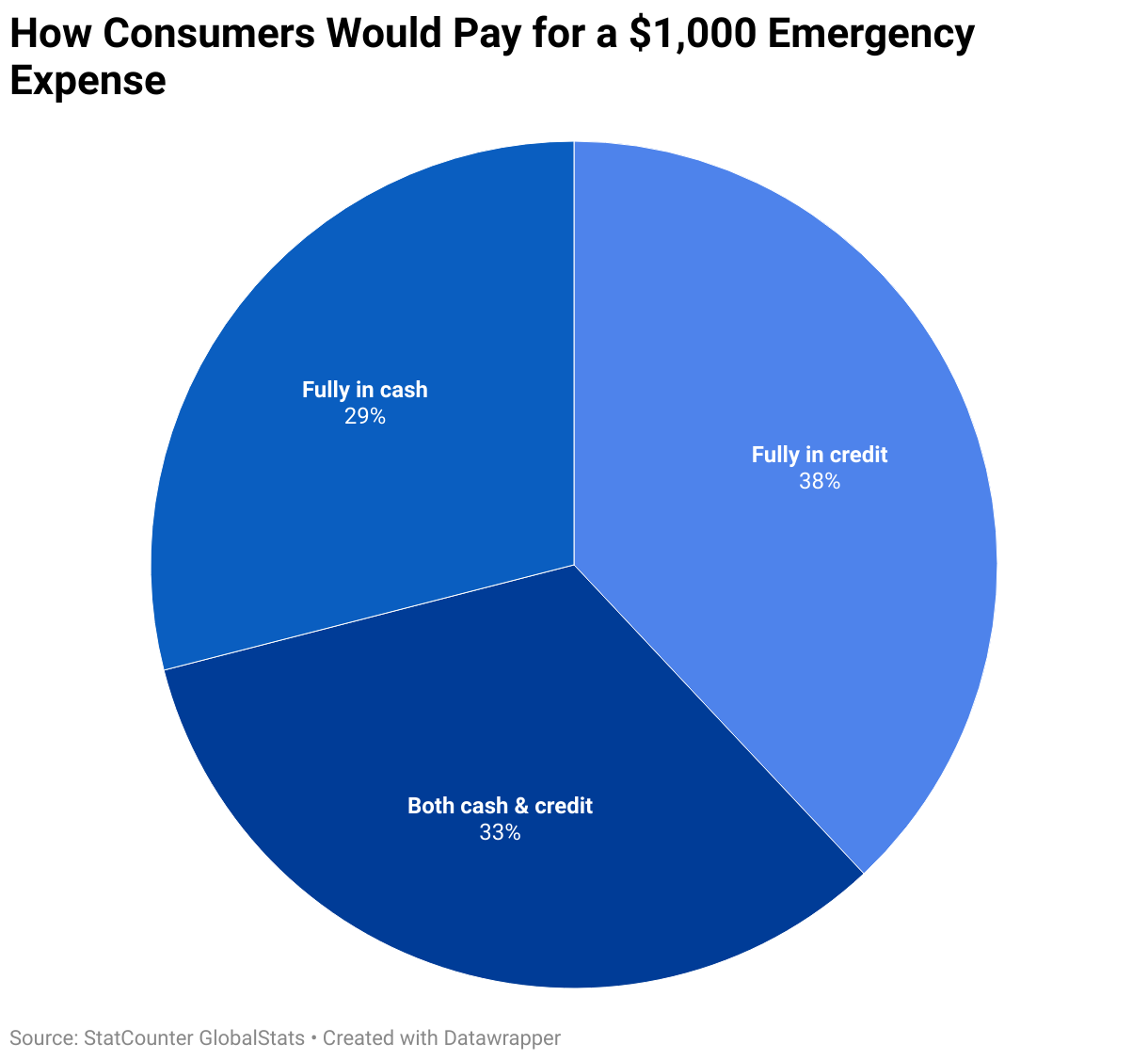

Consumers Claim To Prefer Cash — But Credit Is the Real Safety Net

Most consumers (60%) still prefer to rely on cash during financial emergencies, but 2 in 5 say they’d turn to credit instead.

Men are more likely than women to rely on cash in a financial emergency (64% vs. 56%), while women are more likely to turn to credit cards (44% vs. 36%). Relationship status may also play a role: 41% of single consumers say they’d reach for a credit card first, slightly more than married respondents (38%).

While most consumers say they prefer to use cash in an emergency — a sentiment that aligns with the common wisdom to avoid debt — it raises a key question: Does this preference hold up when a real crisis hits?

Most Consumers Would Reach for Plastic To Cover a $500 Emergency

When asked how they'd cover a $500 emergency expense, consumers were nearly split — 51% would reach for a credit card, while 49% would use cash. Gender differences stood out: 55% of women would choose credit, compared to just 47% of men. Gen Z and millennials leaned more heavily on credit, with 60% of respondents under 35 years old — and 70% of students — saying they’d swipe first. Outside of these groups, most demographics were evenly divided between cash and credit.

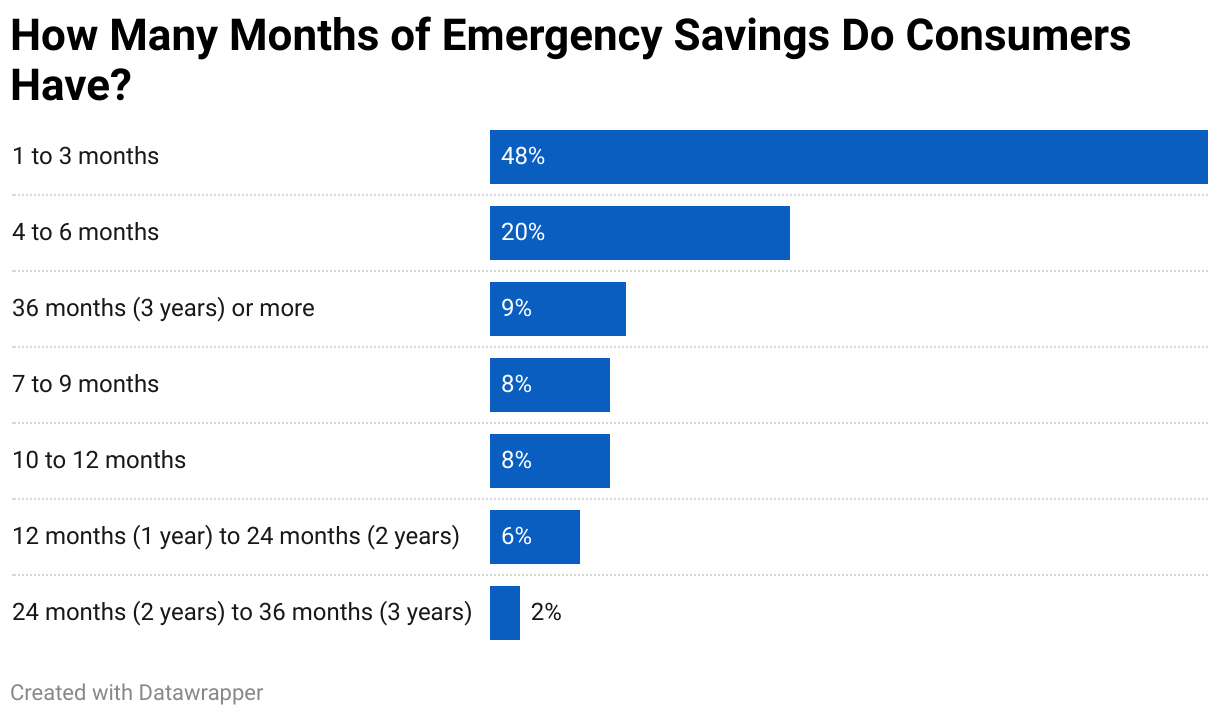

Two-thirds of Consumers Have 6 Months or Less in Savings

Consumers like the idea of using cash for an emergency, but the reality is different.

You’d expect high earners to be better prepared, but that’s not always the case. Just 1 in 4 consumers making over $80,000 have enough savings to cover a year’s worth of expenses, and more than half (56%) wouldn’t last six months. Despite their income, their emergency readiness is only marginally better than average.

Are some generations better prepared for a financial emergency? Baby boomers are slightly better off, with 62% saying they could cover six months or less with their savings. But Gen X is struggling the most — 74% don’t have more than six months saved. Millennials (71%) and Gen Z (68%) aren’t far behind, highlighting a widespread lack of long-term financial security across generations.

Emergency Savings: What We Say vs. What We Have

When it comes to rainy-day expenses, consumers are keeping it simple: 59% prefer cash or debit, and 23% would reach for a credit card. Just 1% said they’d rely on cryptocurrency, proving that even in 2025, no one’s trying to pay for a car repair in Bitcoin.

But preference doesn’t equal preparation. Emergency preparedness is far from universal: 54% of consumers have a rainy-day fund, while 16% say they don’t have one and don’t plan to start one.

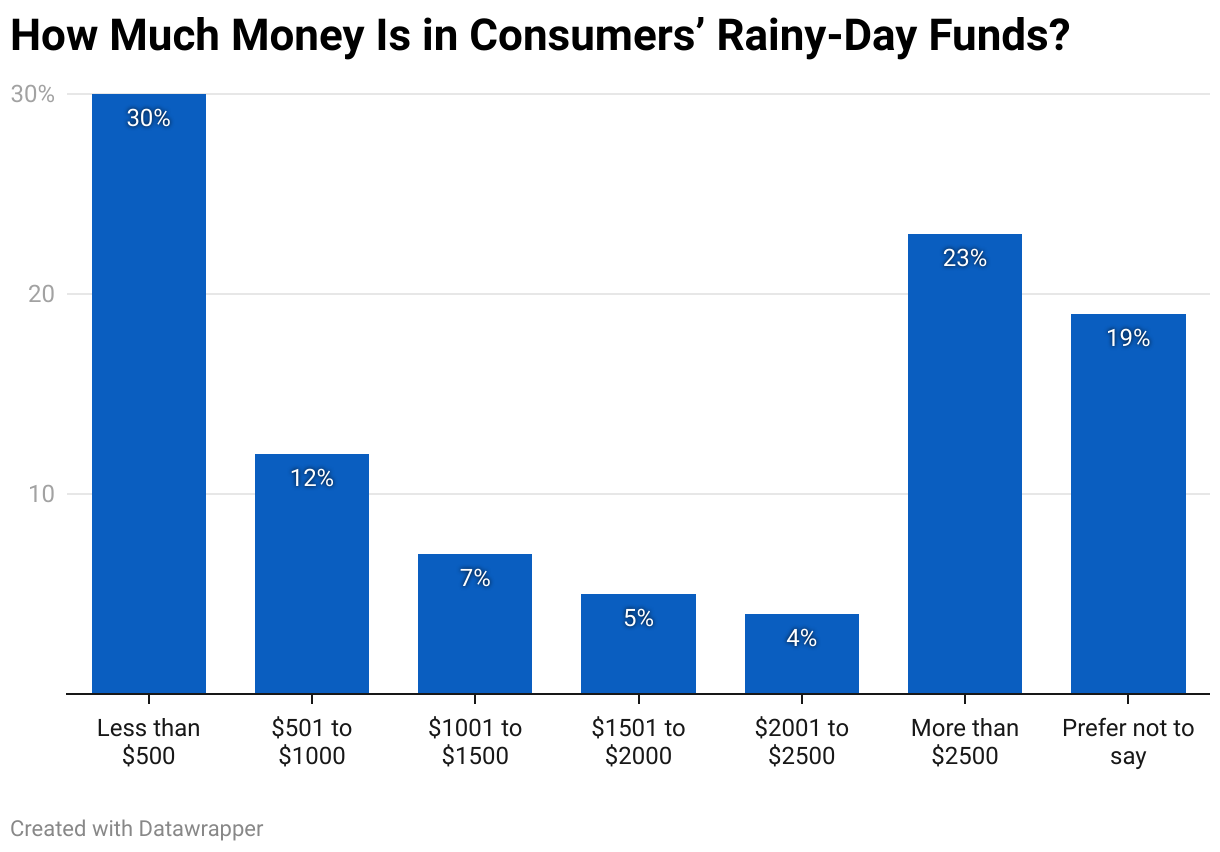

So, how much do consumers have saved for a rainy day?

Married consumers are more than twice as likely as singles to have at least $2,000 in rainy-day savings (37% vs. 17%), suggesting that partnership may offer a financial edge. Age plays a role too: one third of adults 55 and older have hit the $2,000 mark, compared to just 1 in 5 younger adults. Still, despite widespread support for having a rainy-day fund, only 27% of consumers are equipped to cover a major expense without relying on credit.

Younger generations, in particular, are more vulnerable. Only 38% of Gen Zers have emergency cash savings, highlighting how many rely on credit by default, not by choice. In contrast, 65% of baby boomers have cash on hand, reflecting greater financial stability later in life.

Among those who do have a rainy-day fund, nearly half (48%) have $2,000 or more saved, while 32% have less. Gen Xers lead the way in preparedness: 54% have over $2,000 set aside, compared to 46% of baby boomers and 43% of Gen Zers.

Even among savers, many would still struggle to manage a serious emergency. Minor bills might be covered, but bigger costs, like an extended hospital stay or major home repairs, would still push many into debt.

Young Adults Lean on Credit for Financial Security

Nearly 4 in 10 consumers say they want a higher credit limit to cover emergency costs, but that concern isn’t spread evenly. About half of Gen Zers (48%) and millennials (49%) say they need more credit for emergencies, compared to just 27% of baby boomers. The gap emphasizes how limited savings — and greater financial vulnerability — are shaping younger generations’ approach to crisis planning.

Opinions on card limits also support the idea that married people are more ready to deal with emergencies without relying too much on credit. One third of married couples want a higher limit for emergencies, but 45% of singles want an increase.

While credit cards may not be the go-to for emergency spending, 42% of consumers still see them as a financial safety net. That reliance is especially strong among lower-income households — half of those earning under $40,000 say they’d lean on credit in a crisis, compared to just 35% of those making $80,000 or more. Geography also plays a role: nearly half (48%) of urban residents view credit as a backup plan, versus 41% in rural areas and 38% in the suburbs

Gen Z Most Likely To Go Over Their Credit Limit in an Emergency

Faced with an emergency and no available cash or credit, 2 in 5 consumers say they would exceed their credit limit — if their card allowed it — even knowing they’d pay a penalty. Younger adults are far more likely to take that risk: 48% of Gen Zers and 47% of millennials say they’d go over the limit, compared to just 1 in 3 baby boomers. These findings reveal how financial desperation, not recklessness, often drives riskier decisions.

76% of Consumers Don’t Have an Emergency Credit Card

Without cash on hand, credit becomes the default option for handling emergencies. Yet only 1 in 4 consumers (24%) have a credit card specifically set aside for that purpose. For everyone else, everyday-use cards double as emergency lifelines. While many see credit cards as a safety net, few have a dedicated strategy, suggesting most consumers are improvising their way through financial crises as they arise.

Financial institutions have credit card finder tools that people can use to find the appropriate card for emergencies, everyday spending, or a hybrid of both. Meanwhile, pre-qualification can help applicants know which cards they’re more likely to get. This allows people to realistically choose a card that fits their needs and financial situation rather than simply hoping their current credit cards will come through in an emergency.

Gen Z and Millennials Embrace Digital Payments Over Traditional Methods

Consumers have a mixture of payment options in their wallets and on their devices. Here’s what they use for day-to-day spending and emergencies:

Cash: 79%

Debit cards: 78%

Credit cards: 66%

Mobile payments: 31%

Prepaid cards: 24%

Cryptocurrency: 7%

Gen Z and millennials are more likely to hold cryptocurrency than other generations, with 1 in 10 owning some form of digital currency. But that doesn’t necessarily mean they’re quick to adopt other payment technologies. Mobile payment apps, for instance, are more popular among Gen X (36%) and millennials (38%), with lower usage among Gen Z and baby boomers (both around 1 in 4).

Credit cards also show a generational divide. Just 48% of Gen Zers carry a credit card, compared to two-thirds of millennials and Gen Xers, and three-quarters of baby boomers.

When it comes to income, the gap isn’t in preference — it’s in access. Higher earners don’t necessarily pay differently from others; they simply have more ways to make everyday and emergency payments.

While consumers understand that having a cash-based rainy-day fund can help deal with emergencies and avoid potential debt problems, they struggle to create an emergency account with a high enough balance and often have to rely on credit cards as a financial safety net.

Find the full survey and responses here.

1Methodology

This study draws on responses from 1,150 participants across the United States. Our sample included men and women from a range of age groups, income levels, and geographic regions.

We asked participants about their current financial situations, how they handle unexpected expenses, and their plans for managing emergencies in the future. The diverse demographics of our respondents allowed us to explore both national trends and key differences between groups, providing a well-rounded view of consumers’ rainy-day funds and emergency saving habits.

To ensure reliable data, we confirmed that participants had access to all major payment methods (credit, debit, and cash) when answering relevant questions.

Fair Use Policy

Readers are welcome to use the analyses and findings from this study for noncommercial purposes, such as academic research, educational presentations, and personal reference. However, when referencing or citing this article, please ensure proper attribution. Direct linking to this article is permissible and encouraged to provide readers with access to the primary source.

For commercial use or publication purposes — including but not limited to media outlets, websites, and promotional materials — please contact the authors for permission and licensing details. We appreciate your respect for intellectual property rights and adherence to ethical citation practices. Thank you for your interest in our research.